HOW MANY RECESSIONS DID WE REALLY HAVE?

George Kerevan on the black art of economic forecasting…

THE big news from last week – apart from the ever dizzying rise in equity prices – is that the Office of National Statistics has been working its statistical magic once again and made last year’s recession disappear.

Originally the ONS data suggested the UK was in double-dip recession for a nine-month period from the last quarter of 2011 to the middle of 2012. But the latest revised numbers from the ONS show that the construction sector did not contract quite as badly in the first quarter of 2012 as previously indicated. Instead of construction declining by 5.4 per cent, it fell by “only” 5 per cent.

However, as those of you good at mental arithmetic will have worked out, that means the ONS revised its construction industry numbers by 8 per cent, a hefty margin; enough, in fact, to imply that instead of the economy in Q1 of last year being in recession, it actually grew by a whisker.

So, no recession then.

Of course the ONS religiously points out the crudeness of its initial estimates. Everyone knows that it can be several years before the true growth picture emerges - especially economic movements are marginal. However both politicians, the media and (never forget) the markets like certainty. So they seize on every scrap a new data even when everyone knows that data is suspect. Don’t expect that to change.

For the record (and in self defence) this particular column has been arguing for some considerable time that the UK economy has flatlined. Quarterly changes in GDP – up or down – are so small as to be irrelevant.

The key issue is that for several years the economy has been stuck in neutral. As a result, we are still below the peak output of 2008 after five years. Such a prolonged failure to recover trend growth is highly unusual in the post 1945 period. That is what is significant – not the ringing of the quarterly ONS bells.

The political, media and market obsession with the quarterly GDP numbers also raises another (but related) issue – the general uselessness of all long-range economic growth forecasts. Not only is it difficult to find out where the economy has been, it is next to impossible to figure out where it is going!

Every attempt to review the success or failure of economic forecasting models comes up with negative results. But there is something even weirder involved.

Unlike weather forecasting, which is getting more accurate, economic forecasting seems to be getting worse.

The economist and respected Financial Times columnist John Kay explains this as the result of a growing herd instinct: if you have one economic forecaster’s opinion, you have them all. So if the economy changes step unexpectedly, everyone is wrong.

According to Kay, some academic forecasters used to be better than City ones because they were willing to think out of the box – the mavericks. But now there are almost no independent academic forecasters around. Instead, funding for maintaining economic forecasting models comes from commercial sponsorship. The result is not bias but rather an emphasis on consensus. Forecasters and City analysts (and economic commentators such as myself and Bill Jamieson) all talk to each other endlessly. The “conventional wisdom” has a bad habit of dominating thinking, even if you try to avoid it.

And the (insidious) conventional wisdom is that the economy will always revert from where it is presently back to its trend level.

Here’s the rub: if you implicitly assume the economic elastic band will spring back to where it was, you will be useless at understanding what happens if the elastic band suddenly breaks.

Which is where the British economy is now.

Consensus forecasting produces curious results. It can give a false sense of accuracy – temporarily – if the economy grows around trend levels for a while. UK trend growth (till 2008) used to be 2.5 per cent per annum. In the Noughties, if you forecast growth roughly at that level, you looked wonderfully accurate and so garnered headlines and more sponsorship for running your econometric model. In reality the economy was sticking to the train tracks so it accidentally coincided with the forecasters’ consensus. Then came the Credit Crunch and the train jumped the tracks.

True to form, in the aftermath of 2008, forecasters (particularly at the Treasury) simply assumed trend growth would return quickly. That is why Chancellor Osborne thought he could balance the books with little pain. Sadly, the economy has not returned to “normal” and growth has flatlined – meaning tax receipts have nose-dived.

The UK experience is not unique. Recently the Harvard University economist Jeffrey Frankel did a comprehensive review of the reliability of forecasting. He looked at data from 33 countries and found a systematic bias toward over-optimism in official forecasts of GDP and budget balances.

For anoracks, Frankel’s paper indicates that the average upward bias in official forecasts of the budget balance, relative to the realized balance, is “0.2 percent of GDP at the one-year horizon, 0.8 percent at the two-year horizon, and 1.5 percent at the three-year horizon.” Interestingly, Frankel found that the US is more over-optimistic than most other countries: “Official forecasters … over-estimate the permanence of the booms and the transitoriness of the busts.”

Why is weather forecasting more accurate that economic forecasting?

Meteorologists have achieved this partly through increasingly complex computer models, but mainly by going back and checking how their old predictions went. Essentially they look at all previous forecasts (e.g. "there is a 60 per cent chance of rain") and if it rained on 95 per cent of those days instead, then they know they've got it wrong. So they build in a routine to compensate in the future.

This is called calibration and it is rare in economic forecasting.

However, meteorologists don’t have to contend with politicians or the markets – at least to the same degree. Everyone wants economic certainty. So though the ONS can explain till its blue in the face that its quarterly GDP estimates are crude and subject to revision – those crudities will still be tomorrow’s headlines.

SCOT-BUZZ special: A new word for our times

Every once in a while somebody gets it right.

This is not yet found in the Oxford dictionary.

So it was “Googled” and discovered to be a recently “coined” new word found on T-shirts on eBay.

Read this one over slowly and absorb the facts that are within this definition!

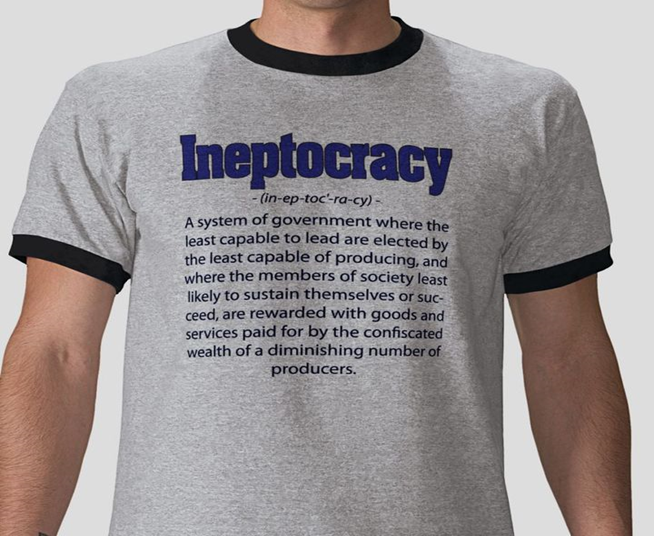

INEPTOCRACY

‘A system of government where the least capable to lead are elected by the least capable of producing, and where the members of society least likely to sustain themselves or succeed, are rewarded with goods and services paid for by the confiscated wealth of a diminishing number of producers.’

We love this word and believe that it will become a recognised English word.

How well it describes our Future.

A perfect fit for our times.

A very happy Christmas and prosperous New Year to all our readers. We will be back in January.

Economy Forecast

09 Jan

- Thursday

- Sunny

- Fri

- Sat

- Sun

- Mon

- Tue

- Wed